Compound interest easily explained

1.- "Let your money work for you"

“Earn money without having to work for it” – Sounds too good to be true. The idea behindCompound interest is one of the most powerful basic concepts of the financial universe.. Albert Einstein is said to have called this effect the eighth wonder of the world and added that those who know about this effect earn money and those who do not understand it pay money. It seems reason enough to look at this effect more carefully.

The idea behind the concept of the effect of compound interest is very simple, it is about making money with money or, in other words,let money work for you. Many people are familiar with the term compound interest, but underestimate its powerful effect and therefore misapply it.

2.- Simple interest vs. compound interest

Let's see with a simple example how compound interest works compared to simple interest. So that you can better follow this example, we have put at your disposal acompound interest calculator.

Suppose we have two people, Pedro and Pablo. Both have €1,000 to invest. We are going to assume that Pedro and Pablo are neighbors and decide to invest said assets in the same financial assets and that they logically obtain the same interest, which we are going to say is 7%. After the first year, both Pedro and Pablo have obtained the same interest of €70. How these interests are calculated is very simple, multiply the money invested by 1.07, 1 by €1,000 and 0.07 by 7% interest. Pedro does not reinvest the interest earned each year and spends it to treat himself while Pablo decides to reinvest it. Pedro is the exemplification of simple interest and Pablo of compound interest. In the second year, Pedro gets €70 again and with the €70 of the first year, he would already have earned €140 in interest. Pablo, for his part, obtains €1,144.9 at the end of the second year as a result of multiplying the €1,070 invested by 1.07. Of these €1,144.9, €1,000 correspond to the initial money and €144.9 to interest. The effect of compound interest has made Pablo earn €4.9 more in that second year than Pedro, sincethe intereststhat Pablo has reinvestedthey generate more interest. For the following year, Pablo will invest the €1,000 again with the €144.9 interest. Since it may take us some time to do these calculations for each year, we are going to skip to the tenth year. Here Pedro will continue to obtain €70 of interest and will have accrued €700 in interest over the ten years. Pablo will have €1,967.15, of which €1,000 are the initial capital contributed and €967.15 are interest. If we jump to the twentieth year, the difference between the benefits of Pedro and Pablo increases. Pedro will obtain another €70 that year and will bring a total of €1,400 obtained in benefits. Pablo will have a capital of €3,869.68 of which €2,869 are profits produced by interest. In other words, thanks to the effect of compound interest, Pablo will have obtained more than twice the benefits that Pedro did.

After this example we see that while Pedro always gets the same thing every year, Pablo's interest increases. If Pedro does not change his strategy, his profits will never grow and they will not produce more than €70.

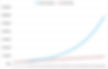

This example serves simply as an example to simply explain the effect of compound interest. Obviously with €3,869.68 in 20 years we are a bit far from being millionaires. In this example we have only invested an initial capital of €1,000 and nothing else afterwards. Let's see this example in a much more graphic way:

Comparison of compound interest vs. simple through the evolution of €1,000 over 50 years with 7% annual interest

In compound interest, the new interest generated increases the capital in each period, while in simple interest this is not the case, interest is always calculated on the initial capital and therefore you will always receive the same amount of interest. Therefore, simple interest does not allow geometric growth. However, in compound interest, interest is capitalized and taken into account for the next interest calculation.

3.- The most important elements of compound interest

The effect of compound interest depends a lot on the factors time and invested capital. If, for example, at the age of 25, once you have finished university and found your first job, you start saving and investing €150 each month with a fixed interest rate of 7%, then when you reach 65 your savings will have grown to almost €400,000. If you invest the money without using the effect of compound interest, you would only have €173,000. The effect of compound interest has contributed almost a quarter of a million euros to your capital.

If instead of €150 you manage to save and invest €400 a month, at the age of 65 you will have a little more than 1 million euros, you will be millionaires! If you now invest that million euros in less risky assets, which provide you with 5% interest, you will have a pension of approximately €4,100 every month simply with interest.

What we can see is thatthe earlier you start investing and the higher your monthly savings rate, the greater the benefit of the compound interest effect. And maybe you are thinking, “Invest now? If I barely earn money, I better wait until later when my economy improves. If you think like that, you have the typical mindset of people who miss out on the power of compound interest. In this case, the saying "Never leave for tomorrow what you can do today" applies very well, since everything that is postponed ends up being forgotten. What is the error then? The failure in the way of thinking is to postpone investing for not having money, whenthanks to investing more money is generated.

In the examples in this article, we are using a constant interest rate of 7% every year. This interest is indicative. In real life our investments do not have a constant interest rate, everything will depend on the financial asset in which you invest. Right now we are in a very low interest phase and you will surely wonder: Where do I get 7% interest today? We will discuss this topic in later articles. Here we want to explain as simply as possible the power of compound interest. In any case, 7%, although it is indicative, is not far from reality. Two of the most representative indices worldwide are the S&P500 and the MSCI World, and they have averaged returns of more than 9%. There will be years in which the result is positive and others in which it is negative, but on average in the long term it is usually around 9%. Hence, we have used the value of 7% (somewhat more conservative), since our intention is to invest in the long term.

In the examples we have not taken into account taxes, inflation, transaction costs or costs intrinsic to the portfolio. Each country has a different tax system and taxes can vary each year, as can inflation. In any case, this should not be an excuse for not investing, since inflation will affect you yes or yes, it does not matter if you invest or not and taxes are only paid on capital gains, that is, on the benefits obtained from investing. . The transaction costs and the intrinsic costs of the portfolio are a last but important factor that plays against you in the effect of compound interest. If you have a portfolio of securities with high intrinsic costs or you brokerIt charges you high transaction costs every time you buy or sell, you will have to pay a percentage in fees each year that will greatly reduce the profits that the compound interest effect has provided you.

4.- Importance of the timing of interest payment

We are now going to explain another of the factors that strongly influence the effect of compound interest. The frequency in which interest is distributed plays a very important role since, in compound interest, the interest you receive is reinvested as soon as it is received. Let's see with a simple example, that it is better to receive interest quarterly or even monthly than annually. Suppose we invest €1,000 with an annual interest rate of 7%. At the end of the year we get €70. We are going to see how the interest rate changes if instead of receiving a single payment at the end of the year, we receive interest quarterly, that is, four times a year. The resulting interest rate will be higher than 7%, since more interest is generated on the interest we earn in the first quarter in the second, third, and fourth quarters. Interest in the second quarter generates more interest in the third and fourth quarters, and so on. Therefore, the effective interest rate when interest is distributed each quarter will be higher than the annual interest rate of 7%. To find out what this effective interest rate is, we divide 7% annual interest by 4, the number of quarters in a year, and we see that the interest rate for each quarter is 1.75%. If we now want to calculate the compound interest effect from quarter to quarter, we multiply the 1.75% of the first quarter by the 1.75% of the second quarter, the 1.75% of the third quarter, and the 1.75% of the fourth quarter. . Thus, we obtain an effective interest rate of 7.18%. Simply by the fact of not obtaining interest once a year but four times a year and reinvesting it, we have obtained 0.18% more interest.

If we now go further and calculate the effective interest rate when the interest is distributed monthly, we obtain 7.23%, that is, 0.23% more than if we only obtained the interest at the end of the year. For this reason, the frequency with which interest is distributed throughout the year is quite important.If you are faced with the choice of two identical financial products that only differ in the frequency of interest payments, always choose the financial product that pays interest at shorter intervals..

If you now think in debts or bank credits, you will realize that this factor plays against you. The more frequent the interest payments to the bank, the greater the negative effect on your debts, since you will be paying interest on interest. This effect is very powerful for those who save, but counterproductive for those who pay debts. We thus return to the quote by Albert Einstein, who said, those who understand compound interest earn money and those who do not, pay money.

5.- Conclusion

Summing up, we can say that the effect of compound interest has a huge impact on your investments. If you earn interest ordividendsof yoursActions, reinvest that money instead of spending it, otherwise your assets will not grow exponentially. Use the eighth wonder of the world to grow your wealth. On the other hand, compound interest has a negative impact when you are in debt. Therefore, try to get rid of expensive loans such as consumer loans or overdraft loans as soon as possible and start saving as soon as possible.

We have designed a compound interest calculator so that you can enter your data yourself and see how "powerful the magic of compound interest is". To go to the calculator, use thislink.